Chipsets, known as graphics processing units (GPU), are probably the most important device that is now in the development of generic AI. Investing in semiconductor shares over the past few years has been a great idea, as you are almost guaranteed a certain way of impact of GPUS or data centers.

However 2025 did not fall into the best start of chip shares.

Whether it is a drama brought to the Chinese start Rearing giftingUS President Donald Trump’s new tariffs or high investor expectations, many names in the chip in the chip have not been so good this year. Macro point of view, Vanech semiconductor and F Decreased by 4% in 2025 (as of March 3). When it comes to specific companies, take Nvidia aeration of Advanced micro deviceswho have seen their shares with 7% and 17%, respectively, so far this year.

Although many investors do not seem to be of Nvidia or money, there is another share that has been captured in a semiconductor landscape, and I think it’s worth immersement now.

Let’s study why it looks like a profitable opportunity to buy now Taiwanese semiconductor production(NYSE: TSM) stock hand with a fist.

When the brand recognition in the chip market is not needed to look much further than Nvidia and the dram. These two crushers are charged with GPU Revolution. Whereas Broadband Playing a special role in outfit in data centers, advanced Chipware, while Micron technologyHigh and more important memory storage solutions are more and more important, as AI Data Cargo becomes larger and complicated.

The titles and spoken items are predominant with so many other names, I would not be surprised if you are not even aware of Taiwan’s semester or TSMC. The point is that many leaders in the chip space, including NVIDIA, AMD and Broadcom, must succeed in the semester of Taiwan.

TSMC specializes in casting solutions that are mainly a fantastic term, which means that it actually produces chips and integrated systems for semiconductor companies. In other words, without TSMC, NVIDIA’s chip architecture would be more idea than tangible products.

Taking into account how much the GPUs have occurred for the last few years, it should not be surprised that the semi-income and profit of Taiwan are growing. In this way, I think that the company’s growth is just starting to hit the gear.

Most of the “Great Seven” companies such as Microsoft:To be in style ContricolativeTo be in style Alphabetand Meta Platforms:The Customs Silicon is being studied as a strategy to migrate from the Chipware overcrowding of NVIDIA. These great technology giants, as well as a traitor manufacturer OpenIt is reported that they are cooperated with TSMC to help bring their visions to life.

Although TSMC has already acquired almost two-thirds of the possibility of the foundry market, I think the advent of the more customs silicone, except for the next two years, and over the next few years.

Image source: Getty Images.

Despite the position of a strong TSMC market and strong financial worldview, the shares of chip shares are cheap.

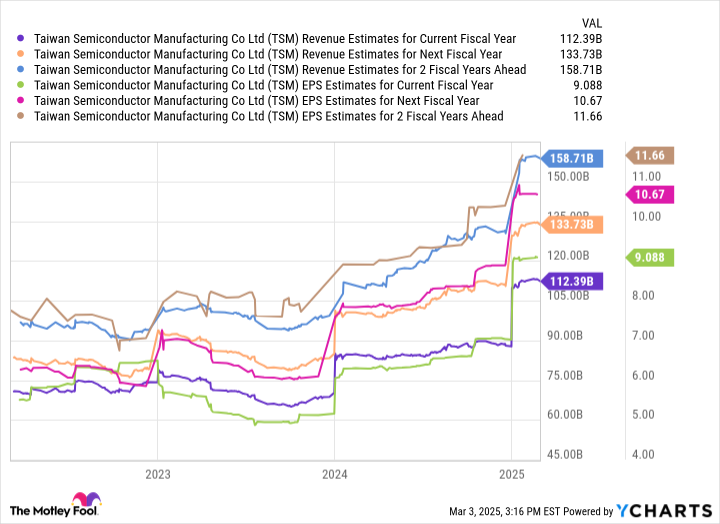

Right now, the middle lead price (P / E) for multiple S & P 500 It’s about 21. Since the table above shows: The semi-annual P / E of Taiwan is approximately 19. For me, this disproportion can also see greater risky, which are also bigger.

My eyes, the two main risks spinning about investments in TSMC are as follows:

The semiconductor industry is cyclic.

Geopolitical tension between China and Taiwan.

Although I can understand those points in a scientific sense, I think that fear over those topics is overlooking. The demand for chip will soon be expected at any time, as the market predicts that in the next decade it increases and reaches almost $ 1 trillion.

TSMC actions on top of it are not exceptional for Taiwan. In fact, the company simply announced in early March that it will invest $ 100 billion in the United States to expand its production footprint. This seems to spend more than $ 300 billion in 2025.

I think the TSMC fund is a transaction right now. Long-term investors may want to take into account the hands of this stock, before the company’s production witnesses even the further scale, as the AI revolution continues to be completely steamed.

Before buying shares, consider Taiwan’s semiconductor production, consider this.

Is MOTLEY FOOL STOCK ADVISOR Analyst team just found out what they believe 10 Best Shares: To buy investors now … and Taiwan’s semiconductor is not one of them. The 10 shares performing the cut can return to the monster in the coming years.

Consider when Nvidia This list did on April 15, 2005 … If you have invested $ 1,000 at the time of our proposal, You will have $ 677,631! *

Now it is worth mentioningStock Consultant:Total average return822% – Market crushing excellence166%For S & P 500. Don’t miss on the last 10 lists available when joiningStock Consultant:A number

John Makay, the former General Director of the All Food Market, is a member of the Board of Directors of Motley Fool. RANDI UCK UCKBERG, Former Market Development Director and CEO of Facebook and Sister Mark Zukeberg is a member of Motley Fool’s board. The Executive Susan Frait, Executive Susan Frait, is a member of the Motley Fool Board. Adam Spatacco: It has positions in the alphabet, Amazon, Meta Platforms, Microsoft and NVIDIA. Motley Fool has positions and progresses advanced micro devices, alphabet, Amazon, Meta platforms, Microsoft, Nvidia and Taiwan. Motley Fool offers Broadcom and offers the following options: Motley Fool has Discovery Policy:A number